Posted on 6 Oct 2024

Posted on 6 Oct 2024

104505

104505

WeChat ID :

Login/Register

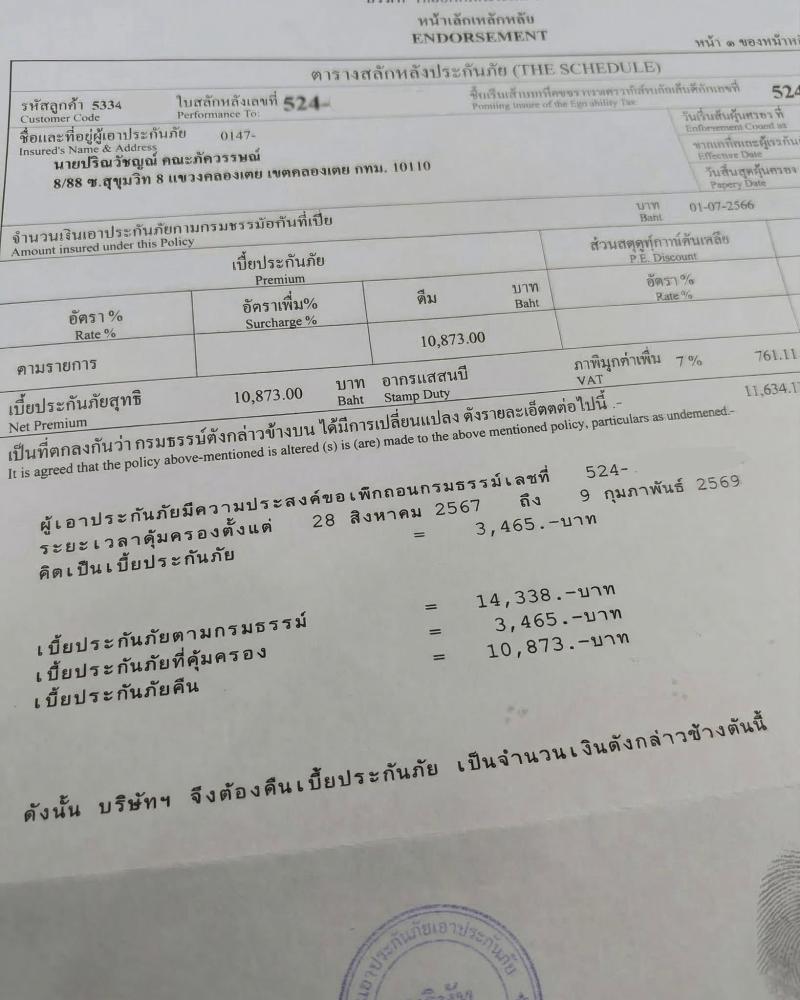

Property owners often focus on the mortgage

tax

and transfer documents when selling.

One item can be forgotten:

the remaining fire-insurance policy.

.

Some mortgage arrangements include multi-year fire coverage.

If the property is sold

the mortgage is discharged

or the insured interest changes before the policy expires

there may be cancellation procedures or an unused-premium amount to review.

.

The owner should contact the insurance company directly and ask:

Is the policy still active?

Can it be cancelled?

Is any premium refundable?

How is the refund calculated?

Which documents are required?

.

Common documents may include

identification

the policy

bank or mortgage-discharge evidence

sale or transfer documents

and the account for receiving payment.

.

The right and amount are not identical in every case.

They depend on the policy wording

remaining term

insurer calculation

and reason for cancellation.

.

Do not assume the policy ends automatically

or that every contract produces the same refund.

Ask the insurer

and keep the response in writing.

Note: This article provides general information. Policy terms and insurer procedures determine the actual outcome.

.

Join the conversation at

https://www.facebook.com/photo.php?fbid=10167241128533696&set=pb.665933695.-2207520000&type=3